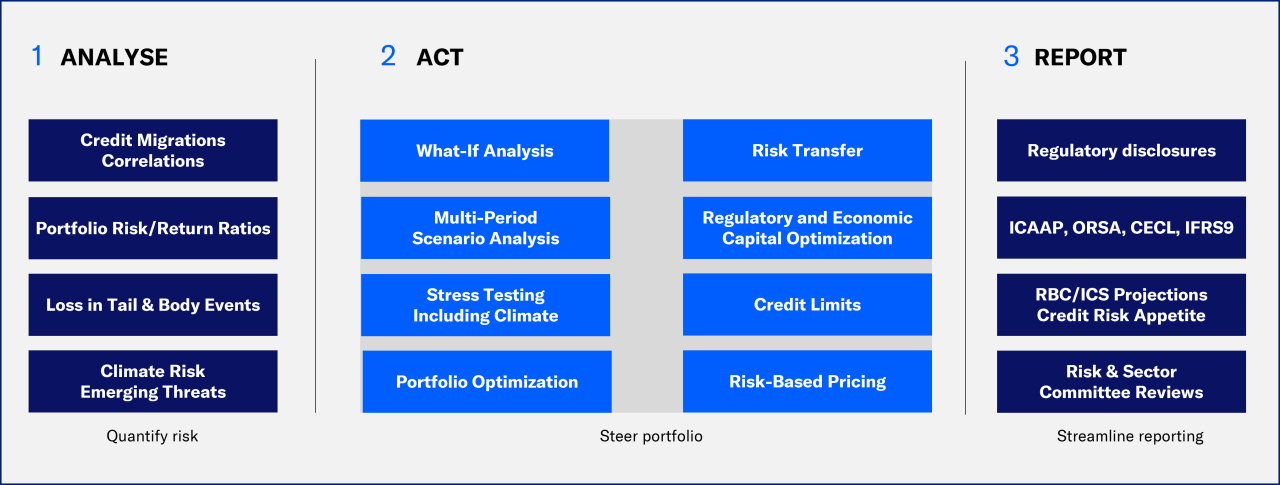

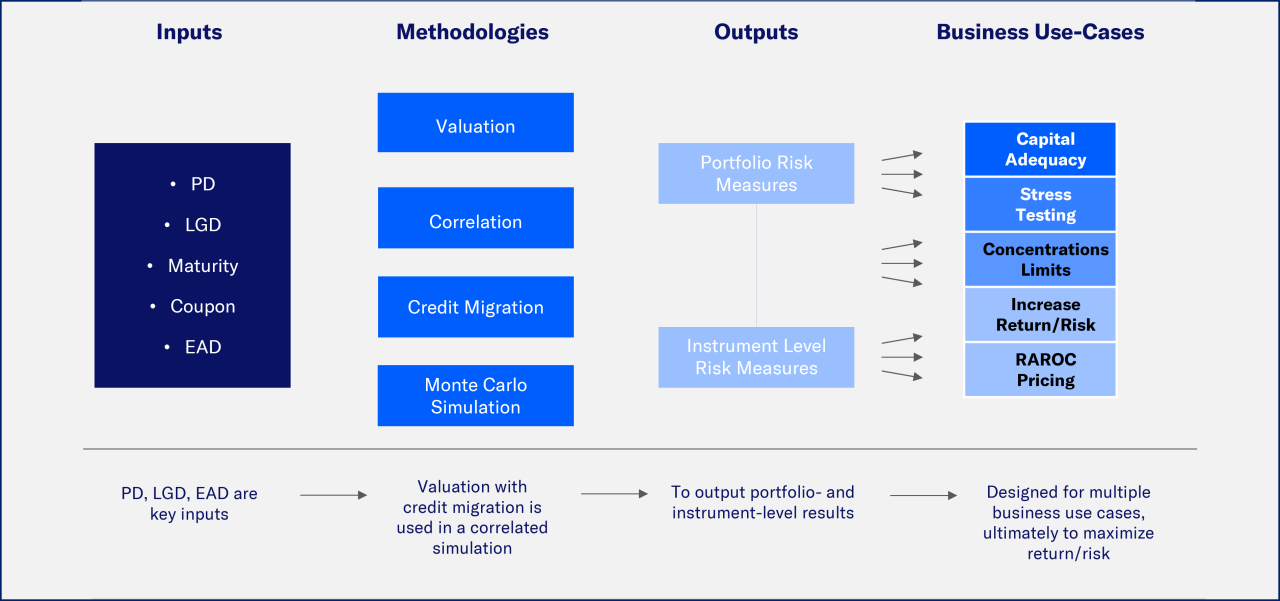

Moody's credit portfolio management solution enables comprehensive portfolio risk analysis, covering concentration, asset correlations, credit risk, physical and transition risk, scenarios, and more.

Credit risk and concentration analysis

Measure and benchmark portfolio-level credit risks and returns across the entire portfolio

Model and assess the impact of credit risk factors, such as pricing models, risk concentrations, correlations, hedging, and stress tests, across portfolios

Estimate asset correlations for publicly traded firms, private firms, retail borrowers, commercial real estate, emerging markets, and more

Anticipate risks with early warning indicators and real-time portfolio monitoring tools